Differences Between Dwelling Fire Insurance and Homeowners Insurance

Updated: March 2026

Navigating the world of insurance can feel like diving into a maze, especially when you encounter terms like “dwelling coverage” and “dwelling fire insurance.” At Portsmouth Atlantic Insurance, we understand the confusion these terms can cause. Let’s break down the differences between dwelling fire insurance and homeowners’ insurance to help you make informed decisions about protecting your property.

Unpacking Homeowners Insurance

When you hear “homeowners insurance,” it’s essential to recognize that it encompasses various coverages within a single policy. While these coverages may vary depending on your specific policy, they typically include:

- Coverage A: Dwelling

- Coverage A protects the structure of your home and attached structures like patios or porches from damage due to covered perils.

- Coverage B: Other Structures

- This coverage extends to freestanding structures on your property, such as detached garages or sheds.

- Coverage C: Personal Property

- Personal property coverage insures your belongings, covering losses caused by covered perils.

- Coverage D: Loss of Use

- If your home becomes uninhabitable due to a covered loss, this coverage reimburses additional living expenses.

- Coverage E: Personal Liability

- Personal liability coverage safeguards you against legal and medical expenses if someone sues you for injuries or property damage.

- Coverage F: Medical Payments to Others

- This coverage pays for medical expenses if someone is injured on your property, regardless of fault.

While dwelling coverage is a crucial component of homeowners insurance coverage options, it’s just one piece of the puzzle.

These policies are built around owner-occupied living.

That assumption influences how liability is handled, how claims are evaluated, and how temporary living expenses are supported.

When a home is no longer used this way, coverage may not respond as expected.

Understanding Dwelling Fire Insurance

Dwelling fire insurance for rental properties, on the other hand, is a separate policy designed for specific circumstances. This structure is often used when the property itself is the primary concern, rather than the lifestyle inside it.

For landlords and property owners, the focus shifts toward the structure, rental continuity, and reduced exposure to occupant-related risk.

Here’s what you need to know:

Purpose and Scope

Dwelling fire insurance primarily targets non-owner-occupied properties, such as rental homes or vacation properties. It provides coverage for the structure but typically excludes personal property and liability protection.

Flexibility

While dwelling fire insurance is commonly used for rental properties, it can also apply to owner-occupied homes, especially those used seasonally or intermittently.

Supplementary Coverage

While the primary focus is on the structure itself, some policies may offer options to include limited personal property coverage or additional liability protection.

Do You Need Dwelling Fire or Homeowners Insurance?

The decision becomes clearer when you align coverage with how the property is actually used:

- Primary residence: Designed for daily living, personal liability, and continuity if the home becomes uninhabitable

- Secondary or seasonal homes: Often require coverage that reflects periods of vacancy and different usage patterns

- Rental or investment properties: Focus shifts toward structural protection, tenant exposure, and protecting rental property income

- Vacant homes: Standard homeowners policies may not respond as expected when occupancy changes, which is why vacant home insurance coverage becomes relevant

- Homes under construction or renovation: Risk profile changes significantly during these phases and may require builders risk insurance coverage and may require different policy structures

The Importance of Location

Your property’s location also plays a significant role. In areas prone to wildfires, flood or other natural disasters, securing adequate coverage, including flood insurance coverage, becomes essential, whether through homeowners or dwelling fire insurance, is crucial.

In New England, this distinction becomes more pronounced.

Properties across New Hampshire and surrounding states often face seasonal occupancy, winter-related vacancy, and storm-driven reconstruction delays.

These factors influence not just underwriting, but how coverage performs during a claim.

Common Coverage Misalignments

Some of the most common issues are not a lack of insurance, but a mismatch between the policy and how the property is used:

- A rental property insured under a homeowners policy

- A seasonal home treated as fully occupied year-round

- A vacant home left on a standard policy

- A landlord assuming liability extends to tenant use

These situations often appear adequate until a claim reveals the gap.

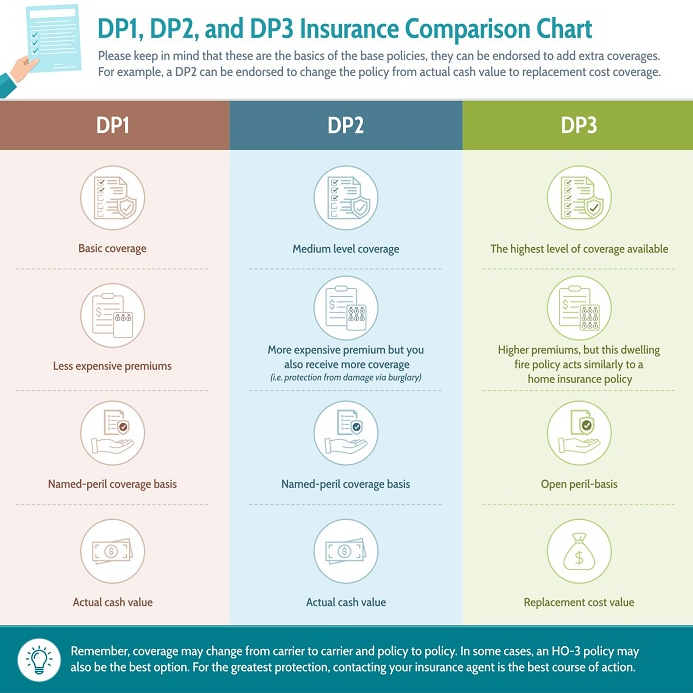

Types of Dwelling Fire Insurance

These are commonly referred to as DP-1, DP-2, and DP-3 policies, each offering different levels of protection depending on risk tolerance and property use.

Dwelling fire insurance comes in various forms, each offering different levels of coverage:

DP-1: Basic Form

- Named perils policy covering basic risks like:

- Hail or windstorms

- Other explosions

- Smoke

- Riot/civil commotion

- Volcanic eruptions

- Aircraft or vehicles

- Typically settles claims on an actual cash value basis but may offer options for replacement cost coverage.

DP-2: Broad Form

- Extended coverage as mentioned in the basic form

- Vandalism and malicious mischief

- Weight of ice and snow

- Glass breakage

- Burglary damage

- Falling objects

- Frozen pipes

- Accidental discharge or overflow of water or steam

- Electrical damage

- Collapse

- Loss of rent coverage in the event tenants are required to move out while the landlord repairs the home from a covered loss

- Often settles claims on a replacement cost basis, providing more comprehensive protection.

DP-3: Special Form

- Open perils policy covering all risks except those explicitly excluded.

- Exclusions in a DP-3 policy typically include:

- War

- Laws and ordinances

- Water damage

- Neglect

- Intentional loss

- Gradual issues like mold, rust, and rot

- Earthquakes

- Offers the highest level of coverage for both the dwelling and personal property.

DP-1: Basic Form vs. DP-2: Broad Form vs. DP-3: Special Form

Closing Thoughts

While dwelling fire insurance and homeowners insurance serve distinct purposes, both play critical roles in safeguarding your property and assets. At Portsmouth Atlantic Insurance, our team of licensed agents is here to help you navigate these options and tailor coverage to your specific needs. Whether you’re a homeowner, landlord, or property investor, we’re committed to providing the guidance and support you need to protect what matters most.

By understanding the nuances of each policy type and assessing your unique circumstances, you can make informed decisions to ensure comprehensive coverage and peace of mind for the future. Reach out to us today to learn more about your insurance options and discover the right solution for your property protection needs.

At Portsmouth Atlantic Insurance, we’re dedicated to helping New Hampshire homeowners navigate the complexities of home insurance. If you have any questions or need assistance with your insurance needs, don’t hesitate to reach out to our team of licensed insurance agents. We’re here to help you protect what matters most.

Contact Us today for Auto and Home solutions and learn more about how we can help. Give us a call at 603-431-4020, email at insure@portsmouthatlanticins.com or fill out the form on this page to get started.

Be sure to follow us on Facebook & Instagram to stay up-to-date on the latest news and tips in the insurance industry. We’re always sharing helpful insights and advice that can help you protect yourself and your assets.

We proudly serve residents in New Hampshire, Massachusetts, Vermont, Maine, Connecticut, Rhode Island, New York, Ohio, Illinois & Florida

FAQs: Dwelling Fire Insurance vs Homeowners Insurance

1. What is the main difference between dwelling fire insurance and homeowners’ insurance?

The main difference is how the property is used. Homeowners insurance is designed for owner-occupied homes and includes liability and personal property coverage, while dwelling fire insurance focuses primarily on the structure and is commonly used for rental, vacant, or seasonal properties.

2. When should you choose dwelling fire insurance instead of homeowners insurance?

You should choose dwelling fire insurance when the property is not your primary residence, such as a rental home, seasonal property, or vacant house. These policies are structured for different occupancy risks and may respond more appropriately than homeowners insurance in those situations.

3. Does dwelling fire insurance include liability coverage?

Dwelling fire insurance typically does not include liability coverage by default. Some policies may allow limited additions, but liability protection is not the primary focus. Property owners often need a separate policy or endorsement to cover legal and medical risks associated with tenants or visitors.

4. Is homeowners insurance enough for a rental property?

Homeowners insurance is generally not appropriate for rental properties. These policies are structured for owner-occupied homes, and claims may not respond as expected if the property is rented. Landlords usually need dwelling fire insurance designed for tenant-related exposure and rental income considerations.

5. What do DP-1, DP-2, and DP-3 mean in dwelling fire insurance?

DP-1, DP-2, and DP-3 refer to different levels of dwelling fire insurance coverage. DP-1 covers basic named risks, DP-2 expands coverage with additional perils, and DP-3 offers the broadest protection with open perils, covering most risks unless specifically excluded.

6. Does dwelling fire insurance cover personal belongings?

Dwelling fire insurance generally does not cover personal belongings unless optional coverage is added. The focus is on protecting the structure itself. In rental situations, tenants are usually responsible for insuring their own belongings through renters insurance.

7. Myth vs Fact: Dwelling fire insurance is only for fire damage

Myth: Dwelling fire insurance only covers fire damage.

Fact: While the name suggests fire coverage, these policies can include protection against multiple risks such as wind, hail, vandalism, and water damage, depending on the policy type (DP-1, DP-2, or DP-3).

8. Myth vs Fact: Homeowners insurance always covers vacant homes

Myth: Homeowners insurance automatically covers vacant homes.

Fact: Standard homeowners policies may limit or exclude coverage if a home is vacant for an extended period. In these cases, a dwelling fire or vacant home policy is often more appropriate to reflect the increased risk.