Article updated: March 2026

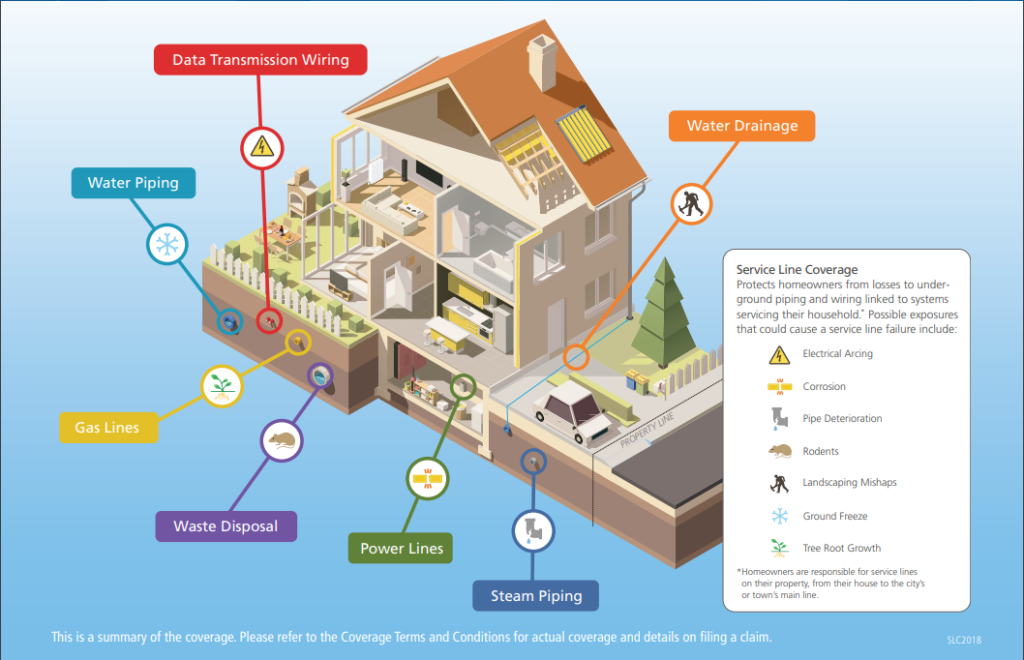

Service Line Coverage

Service lines are easy to overlook because they are out of sight. Yet for many New Hampshire homeowners, they represent one of the more expensive and disruptive types of property damage when something goes wrong.

Water lines, sewer pipes, and underground utilities can fail without warning, often requiring excavation, repair, and restoration of the property. These costs are typically not covered under a standard homeowners policy.

Service line coverage is designed to address this specific gap, helping homeowners manage the financial impact of underground utility damage in a more predictable way.

What is Service Line Coverage?

Service line coverage is an optional endorsement added to a homeowners insurance policy that covers damage to underground utility lines that covers damage to underground utility lines on your property, including water, sewer, electrical, and other service connections. These service lines can include power lines, phone and cable lines, water and sewer pipes, and more. It typically includes the cost of excavation, repair, and in some cases restoration of landscaping when a covered service line failure occurs.

Why Do You Need Service Line Coverage?

Many homeowners assume that utility companies are responsible for damaged lines. In most cases, responsibility begins at the point where the line enters your property, leaving the homeowner responsible for repairs.

Standard homeowners insurance typically excludes damage to underground service lines, which becomes clearer when reviewing how policies are structured in a broader New Hampshire home insurance guide unless additional coverage has been added.

With service line insurance in place, coverage may extend to excavation, repair, temporary loss of service, and restoration of the affected area, depending on how the endorsement is structured.

Many homeowners only recognize this gap after a loss, similar to how gaps appear with water backup coverage when protection hasn’t been reviewed in advance, when access to the damaged line becomes the most expensive part of the repair.

Understanding Service Lines

Service lines encompass various utilities and infrastructure on your property. Here are some examples of service lines:

- Power lines and electrical wiring

- Steam piping

- Telephone and cable lines

- Drainage

- Fuel lines

- Water pipes

- Waste disposal

- Sewer piping

- Private wells and septic systems

Causes of Service Line Damage

Service lines can be damaged by a variety of factors, including:

- Rust or corrosion

- Ground freeze

- Tree or other root invasion

- Landscaping accidents

- Rodents

- Wear and tear

- Mechanical breakdown

- Collapse from aboveground weight

- Artificially-generated electric current

- Freezing or frost heave

- In some cases, water-related damage may overlap with risks typically addressed through flood insurance, depending on how the loss occurs.

Cost of Service Line Repair

The average service line repair can range from $3,000 to $4,000, but costs can escalate depending on the affected line and the extent of the required repair.

What Service Line Insurance Covers

If a service line on your property is damaged by a covered cause of loss resulting in a service failure, your service line endorsement on your homeowners policy will pay up to the limit of coverage on your policy for the cost of repair.

How Much Does Service Line Coverage Cost?

The cost of service line insurance coverage varies depending on several factors. Coverage structure and limits can vary between policies. Reviewing how service line coverage fits within your broader homeowners insurance often brings more clarity than focusing on cost alone.

Key Details About Service Line Coverage

- On-Premises Requirement: The affected service line must be located on your premises and provide a service to the residence or related covered private structures to be covered.

- Green Replacement: Some insurance companies will pay up to 150 percent of the cost of replacement with environmentally-friendly materials if a covered service line requires replacement.

- Deductible: vary by policy, though many service line endorsements include a per-occurrence deductible that applies specifically to this type of loss.

- Coverage Extension: The service line coverage endorsement extends coverage for breakage caused by the weight of equipment, animals, or people, and may also apply if you crush a service line while digging in the yard.

Is Service Line Coverage Worth It?

When evaluating service line coverage, the consideration is less about frequency and more about severity.

These events are relatively uncommon, but when they occur, they tend to be disruptive, invasive, and costly. It ensures that you’re not left paying for costly repairs out of pocket, giving you peace of mind knowing that your home and finances are protected.

Conclusion: Secure Your New Hampshire Home with Service Line Coverage

Service line failures are not always visible until they become urgent. With service line coverage from Portsmouth Atlantic Insurance, you can rest easy knowing that your New Hampshire home is well-protected against the financial repercussions of service line failures.

Give us a call today to speak with one of our licensed agents and explore your options for service line coverage. Protect your home and your peace of mind with Portsmouth Atlantic Insurance.

FAQs About Service Line Coverage

1. What does service line coverage actually cover?

Service line coverage pays for the cost to repair or replace damaged underground utility lines on your property, including water, sewer, electrical, and communication lines. It often includes excavation and restoration costs, which are typically not covered under a standard homeowners insurance policy.

2. Is service line coverage included in standard homeowners insurance?

No, service line coverage is not included in most standard homeowners insurance policies. It is usually offered as an optional endorsement that must be added separately. Without it, homeowners are typically responsible for repair and excavation costs when a service line fails.

3. How much does it cost to repair a service line without insurance?

Service line repairs typically cost between $3,000 and $4,000, though costs can increase depending on the type of line and extent of damage. Expenses often rise due to excavation, labor, and restoration, making uninsured losses financially disruptive for many homeowners.

4. Who is responsible for service line repairs: the homeowner or utility company?

In most cases, the homeowner is responsible for service lines located on their property, especially from the home to the street connection. Utility companies usually only maintain the main lines. This distinction often becomes clear only after damage occurs.

5. What causes service line damage?

Service lines can fail due to corrosion, ground movement, tree root intrusion, freezing, or simple wear over time. External factors like construction, heavy equipment, or shifting soil can also contribute. These issues often develop gradually and are not visible until a failure occurs.

6. Is service line coverage worth it for homeowners?

Service line coverage is often considered worthwhile because failures are infrequent but expensive. The cost of a single repair can exceed several years of premium. For many homeowners, the decision is less about probability and more about protecting against a high-cost, disruptive event.

7. Does service line coverage include landscaping and property restoration?

Yes, many service line coverage endorsements include restoration costs such as repairing driveways, lawns, or walkways after excavation. Coverage details vary by policy, so it is important to review whether restoration is included and to what extent it is covered.

8. Myth vs Fact: “New homes don’t need service line coverage.”

Myth. Newer homes are not immune to service line issues. While materials may be newer, factors like soil conditions, installation quality, and external damage still apply. Service line failures can occur regardless of a home’s age, making coverage relevant even for newer properties.

9. Myth vs Fact: “Service line coverage only applies to sewer pipes.”

Myth. Service line coverage applies to multiple types of underground utilities, including water lines, electrical wiring, gas lines, and communication cables. Sewer lines are just one part of a broader system of connections that can be covered under this endorsement.