At a Glance

If you’re short on time, here’s what to know:

- Many homeowners are also surprised to see their premiums increase over time. Understanding why your homeowners insurance is so high can provide more context behind these rising costs.

- Even if your home wasn’t damaged, widespread losses can influence insurance pricing. Learn more about how claims affect insurance premiums and why rates may increase after major loss events.

- Your premium can increase even if you haven’t filed a claim because insurers also consider broader market trends and regional claim costs.

- Reviewing your coverage regularly can help ensure your policy still fits your home, vehicle, and budget.

- Working with an independent insurance agency allows you to compare coverage from multiple carriers rather than relying on a single insurance company.

Thanks to ongoing economic conditions, higher claim costs, severe weather, and rising repair and rebuilding expenses, many homeowners and drivers are seeing higher insurance premiums when it’s time to renew their policies.

Insurance rates are based on what an insurer expects it will cost to make you whole after a covered loss, whether that’s repairing a roof after a windstorm or replacing a vehicle after an accident. As you’ve likely noticed, rebuilding homes, repairing vehicles, and even medical care all cost considerably more than they did just a few years ago.

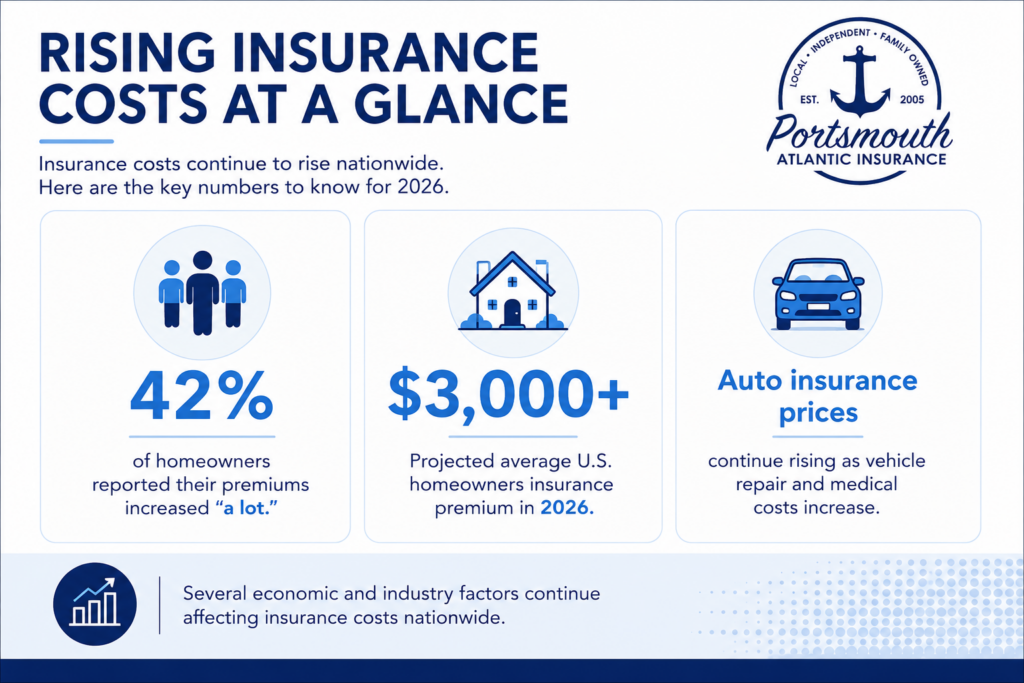

Many homeowners also want to understand what’s causing these increases beyond inflation. Our guide on why your homeowners insurance is so high explores several of the biggest factors influencing today’s premiums., while 42% reported their premiums went up “a lot.” Industry forecasts also suggest the average homeowners insurance premium could exceed $3,000 nationally in 2026, reflecting how dramatically insurance costs have changed over the past several years.

While these trends are affecting homeowners and drivers across the country, New Hampshire residents face some unique considerations. Winter storms, nor’easters, heavy snowfall, coastal weather, and rising local construction costs all influence what insurers expect future claims to cost. Even if you haven’t filed a claim, these broader market conditions can affect your premium at renewal.

One of the biggest misconceptions about insurance is that your premium only changes because of your own claims history. While your individual record does matter, insurers also consider broader factors such as claim trends, weather losses, rebuilding costs, and repair expenses across your region.

Table of Contents

What’s Driving Higher Home Insurance Costs?

Rebuilding a home today costs significantly more than it did just a few years ago. If you’ve hired a contractor or priced building materials recently, you’ve probably seen those higher costs firsthand. Increased material prices, labor shortages, and longer rebuilding timelines continue to make home insurance claims more expensive.

Industry estimates show homeowners insurance premiums have risen significantly since 2021 as replacement costs have increased much faster than overall inflation. Although price increases have moderated in some areas, rebuilding a home remains considerably more expensive than it was before the pandemic.

Severe weather is also playing a larger role. Hurricanes, wildfires, hailstorms, flooding, and severe wind events continue to result in billions of dollars in insured losses every year. Here in New Hampshire, nor’easters, coastal storms, heavy snowfall, and wind damage all contribute to higher claim costs.

Even if you’ve never filed a homeowners insurance claim, your premium can still change. Insurance companies evaluate broader claim trends, not just individual policyholders. As rebuilding costs increase, premiums generally adjust to reflect the higher cost of settling claims.

A policy review can also help you confirm your homeowners insurance coverage still matches your home’s current replacement cost.

What’s Driving Higher Auto Insurance Costs?

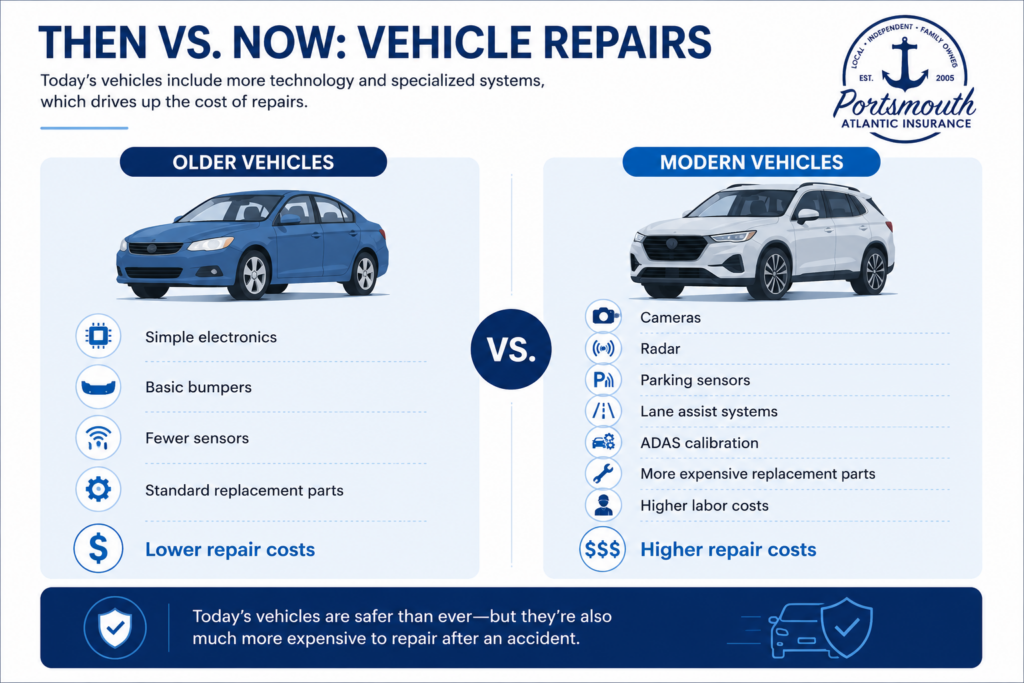

Vehicle repairs have become more expensive as today’s cars include advanced safety systems, cameras, sensors, and other technology that often require specialized parts and repairs. Even relatively minor accidents can result in much larger repair bills than they did a few years ago.

Although supply chains have improved compared to the height of the pandemic, repair costs remain elevated because of higher labor costs, more expensive replacement parts, and increasingly complex vehicles.

Medical expenses also continue to influence auto insurance premiums. As healthcare costs rise, insurers pay more to settle injury claims following an accident, contributing to higher overall claim costs.

According to the U.S. Bureau of Labor Statistics, motor vehicle insurance prices continued increasing year over year during 2026. While some insurers have begun slowing the pace of rate increases, overall insurance costs remain well above where they were just a few years ago.

Why Did My Premium Go Up If I Didn’t File a Claim?

This is one of the questions we hear most often.

Insurance pricing isn’t based solely on your personal claims history. Even homeowners with a clean claims history can be affected by broader market conditions, including what’s known as the insurance hard market, including rebuilding expenses, vehicle repair costs, severe weather losses, and medical inflation.

If those costs increase, premiums may rise even for policyholders with clean driving records and no recent claims.

A premium increase doesn’t necessarily mean you’re paying too much. It may simply be a good opportunity to review whether your policy still fits your needs.

What You Can Do if Your Premium Increases

While you can’t control inflation or severe weather, there are several ways to help manage rising insurance costs. If you’re looking for practical ways to reduce your premium without sacrificing important protection, our guide on how to lower your home insurance offers additional ideas to consider.

- Review your home and auto coverage every year or two.

- Ask about bundling your home and auto insurance.

- Consider whether your deductible still fits your financial situation.

- Make sure you’re receiving every discount you qualify for.

- Update your policy after renovations, home improvements, or major purchases.

If you’re comparing policies, remember that price is only one part of the decision. Coverage limits, deductibles, endorsements, and claims service can vary from one carrier to another. Working with an independent insurance agency gives you the opportunity to compare multiple carriers and choose coverage that fits your needs instead of relying on a single insurance company.

Focus on Value as You Explore Ways to Save

It’s natural to look for ways to lower your insurance costs, but the lowest premium isn’t always the best value.

Two policies with similar premiums can provide very different levels of protection when a claim occurs. Looking beyond price can help you avoid unexpected coverage gaps when you need your insurance most.

If your premium has increased recently, it may be a good time to review your coverage rather than assume your current policy is still the best fit. A policy review may also uncover discounts or identify opportunities to improve your coverage.

Before Your Next Renewal

A higher premium doesn’t automatically mean you need to switch insurance companies. If you’re purchasing a home or recently refinanced, it’s also worth understanding the difference between mortgage insurance and homeowners insurance. In many cases, it reflects broader changes affecting the insurance market rather than your individual policy.

The better question to ask is:

“Does my current policy still provide the right protection for what I’m paying?”

Before your next renewal, take a few minutes to review your policy and consider:

- Has my home’s rebuilding cost changed?

- Have I renovated my home or purchased anything valuable since my last review?

- Does my deductible still make sense for my budget?

- Am I receiving every discount I qualify for?

- Would comparing coverage from multiple insurance carriers give me a better understanding of my options?

If you’re unsure about any of those questions, request a personalized insurance review to compare your current coverage and determine whether it still fits your needs. Sometimes you’ll confirm your current coverage is still the right fit. Other times, you may discover opportunities to improve your protection or reduce your premium without sacrificing important coverage.

At Portsmouth Atlantic Insurance, we work with multiple insurance carriers, giving homeowners and drivers the ability to compare options based on both coverage and value rather than relying on a single insurer.

We proudly serve residents throughout New Hampshire, Massachusetts, Vermont, Maine, Connecticut, Rhode Island, New York, Ohio, Illinois, and Florida.

Frequently Asked Questions

Why did my homeowners insurance go up if I never filed a claim?

Insurance premiums are based on more than your individual claims history. Rising rebuilding costs, severe weather losses, inflation, and regional claim trends can all affect your premium.

Why is my car insurance increasing even though I have a clean driving record?

Your premium reflects broader claim costs, including vehicle repairs, medical expenses, and regional accident trends, not just your personal driving history.

Will home insurance rates go down in 2026?

Some markets may see slower rate increases, but rebuilding costs, weather-related claims, and inflation continue to put upward pressure on homeowners insurance premiums.

Why is auto insurance still increasing?

Modern vehicles are more expensive to repair because they include advanced technology such as cameras, sensors, and driver-assistance systems. Higher medical costs also contribute to larger insurance claims.

Can bundling home and auto insurance help lower my premium?

Many insurance companies offer discounts for bundling multiple policies. An independent insurance agency can help you compare available options.

Does my deductible affect my premium?

Generally, choosing a higher deductible can reduce your premium, but it also means you’ll pay more out of pocket if you file a claim.

How often should I review my insurance policy?

It’s a good idea to review your policy every year or two, or after major life events such as buying a home, renovating, purchasing a new vehicle, or making significant improvements.

Should I shop around before renewing my policy?

Comparing coverage periodically can help ensure your policy still provides the protection you need. An independent agency can simplify that process by comparing multiple carriers on your behalf.

Sources

- CNBC – Homeowners Insurance Coverage and Rising Premiums

- Pew Research Center

- U.S. Bureau of Labor Statistics – Consumer Price Index (Motor Vehicle Insurance)

- U.S. Bureau of Labor Statistics – Medical Care Consumer Price Index

- Insurify – Home Insurance Outlook (2026)